https://ourfiniteworld.com/2020/09/23/reaching-the-end-of-early-stimulus-whats-ahead/

Reaching the End of Early Stimulus – What’s Ahead?

Many people thought that COVID-19 would be gone with a short

shutdown. They also thought that the world’s economic problems could be

cured with a six month “dose” of stimulus.

It is increasingly clear that neither of these assumptions is

correct. Despite the claims of epidemiologists, our best efforts have

never been able to reduce the number of newly reported COVID-19 cases

for the world as a whole for any significant period of time. In fact,

the latest week seems to be the highest week so far.

Figure 1. Chart of worldwide COVID-19 new cases, in chart prepared by Worldometer with data through September 20, 2020.

At the same time, the economy, despite all of the stimulus, is not

doing very well. Airlines are doing very poorly. The parts of the

economy that are dependent upon tourism are having huge problems. This

reduces the “upside” of economic recovery, pretty much everywhere, until

it can be corrected.

Another part of the world economy doing poorly is clothing sales. For

example, many fewer people are attending concerts, weddings, funerals,

out-of-town business meetings and conventions, leading to a need for

fewer “dressy” clothes. Also, with air travel greatly reduced, people

don’t need new clothing for visiting places with different climates,

either. Most clothing is bought by people from rich countries but made

by people in poor countries. This cutback in clothing purchases

disproportionately affects people who are already very poor. The loss of

jobs in these countries may lead to an inability to afford food, for

those who are laid off.

Besides these difficult to solve problems, initial programs set up to

help mitigate job losses are running out. What kinds of things might

governments do, if they are running short of borrowing capacity, and

medical solutions still seem to be far away?

In Section A of this post, I outline what I see as some approaches

that governments might take to try to “kick the can down the road” a

while longer, as well as some general trends regarding near term

outcomes.

In Section B, I explain how our current problems seem to be related

to the more general “overshoot and collapse” problems of many prior

economies. I show that historically, these overshoot and collapse

situations seem to have played out over a number of years. In many ways,

the outcome might look more like “overshoot and decline” than

“overshoot and collapse” from the point of view of an observer at the

time.

In Section C, I explain two different types of “breakage” we can

expect going forward, if we are really dealing with an overshoot and

collapse situation. In the first, oil production is likely to fall

because of the collapse of some of the governments of oil exporters. In

the second, the international trade system breaks down because of

problems with the financial system and countries no longer trusting each

other’s currencies.

[A] Ideas for “Sort of” Addressing the Economic Problems at Hand

The following are a few ideas regarding possible mitigation approaches, and the expected results of these attempted solutions:

[1] Programs to keep citizens in their homes will likely be extended.

Mortgage repayment programs will be extended. Renters will be allowed

to stay where they are, even if they cannot afford the rent.

[2] New programs may be added, allowing those without adequate income

to pay for electricity, heat, water and sewer connections. These

programs may be debt-based. For example, homeowners and renters may be

given loans to pay for these programs, with the hope that eventually the

economy will bounce back, and the loans can be repaid.

[3] More food bank programs will be added, with governments buying

food from farmers and donating it to food banks. There is even an

outside chance that people will be given loans so that they can “buy”

food from the food bank, with the hope that they can someday repay the

loans. All of these loan-based programs will appear to be “cost free” to

the government, since “certainly” the crisis will go away, and

borrowers will be able to repay the loans.

[4] Loans to students will increasingly be put in forbearance, to be

repaid when the crisis is over. Auto loans and credit card debt may be

also be put into forbearance, if the person with the debt has inadequate

income.

[5] Even with all of these actions, families will tend to move back

together into a smaller total number of residences. This will happen

partly because citizens won’t want to be burdened with even more debt,

if they can avoid it. Also, older citizens won’t want to move into

facilities offering care for the elderly because they know that COVID

restrictions may limit who they can have contact with. They will much

prefer moving in with a relative, if anyone will take them in return for

a suitable monthly payment.

[6] As extended families move in together, the total number of

housing units required will tend to fall. Prices of homes will tend to

fall, especially in areas where citizens no longer want to live.

Governments will encourage banks and other mortgage holders to look the

other way as prices fall, but as homes are sold, this will be

increasingly difficult to do. In many cases, when homes are sold, the

selling prices will fall below the balance of the debt outstanding.

Governments will pass laws not allowing financial institutions to try to

obtain the shortfall from citizens, at least until the crisis is over.

[7] Some businesses, such as restaurants without enough patrons and

colleges without enough students, will need to close. Clothing stores

without enough sales will also need to close, as will retirement homes

without enough residents. All of these closures will lead to a huge

amount of excess commercial space. It will also lead to the loss of more

jobs, raising the number of unemployed people.

With these closed businesses, the price of commercial real estate

will tend to fall. Lenders will be encouraged to “extend the loans” and

“pretend that asset prices will soon recover,” when renewing loans. Even

this approach won’t be enough in many cases, as businesses file for

bankruptcy.

[8] With fewer residences and business properties occupied, the

amount of electricity required will fall. Wholesale prices for

electricity will tend to fall, pushing ever more fossil fuel and nuclear

electricity providers out of business. Electricity outages will become

an increasing problem, as renewables become a larger share of the

electricity mix and are unable to increase supply when needed. Rolling

outages will become more common.

[9] Pensions of all kinds will become more difficult to pay.

Government programs, such as Social Security in the US, will have less

revenue to pay pensions. There are funds set aside in the Social

Security Trust Fund to cover a shortfall in funding, but these funds are

simply non-marketable US government debt. In theory, the US government

could add more debt to the Trust Fund and make payments on the basis of

this added debt. Otherwise, the US will likely need to either raise

taxes or increase the “regular” government debt level, in order to

continue to pay Social Security pensions as planned.

Private pensions, backed by bonds and shares of stock (and perhaps

other assets), will find the values of their available assets are

falling. Governments, if they are able to, will try to hide this

problem. For example, regulators may develop a new way to value assets,

so as to make pension funding shortfalls mostly disappear.

In the case of pension bankruptcy, government insurance is often

theoretically available. In the US, Pension Benefit Guaranty Corporation

provides coverage; other countries may have similar programs.

Unfortunately, this program is not set up to handle a large influx of new bankrupt plans,

without raising taxes. The problem then will be raising taxes enough so

that one year’s pension benefits can be paid, pushing the problem down

the road a bit longer.

Bank accounts have similar guarantees, with similar funding problems.

The guarantee organization has very little funds available, without

raising taxes or somehow increasing debt.

[10] Stock market prices will tend to fall, leading those who have

purchased shares using debt to want to sell quickly, pushing the stock

market down further. Currency relativities will fluctuate wildly.

Derivatives of many kinds will encounter payment problems. Many ETFs

likely won’t work as planned. Governments will try to figure out ways to

somehow mitigate these problems to the extent possible. For example,

stock markets may be closed for a time to hide the problems. Or,

additional time may be given to settle purchases, so that perhaps the

deficiencies can be corrected. Eventually, some banks may be taken over

by governments, to assure the operation of the parts deemed essential.

[11] Eventually, governments may find it necessary to nationalize a

wide range of essential businesses. These could range from trucking

companies to banks to oil companies to electricity transmission repair

companies. If the balance sheets of these companies are too bad,

governments may simply stop publishing them.

[12] These types of actions will mostly be available to “rich”

countries. Poor countries can tap their “rainy day” funds, but these

will soon be exhausted. In this case, poor countries will find that

there is little they can do unless international organizations bail them

out. Because of cutbacks in tourism and in orders of finished goods,

such as clothing, these countries are likely to encounter high levels of

unemployment. Without aid, the poorer citizens of these countries will

find it impossible to afford an adequate diet. With inadequate

nutrition, the health of low income citizens will decline, and they will

easily succumb to communicable diseases, such as tuberculosis and

malaria. Death rates are likely to skyrocket.

[B] What Happens When an Economy Outgrows Its Resources?

Most people think that the issue we are dealing with is a temporary

problem associated with a new coronavirus. I think that we are dealing

with a much worse problem: The world’s population has outgrown the

world’s resource limits. This is why our current problems look so

difficult to solve from a financial point of view. This is part of the

reason many people feel that shutting down the economy for COVID-19 is a

good choice. There are really many reasons for the shutdowns, besides

preventing the spread of COVID-19: Keeping people inside stops the many

protests related to low wages. The shutdowns appear to restore order to a

troubled system. Broken supply lines from shutdowns elsewhere reduce

raw materials availability, making it more difficult to keep production

in one part of the world operating, when others are closed.

Overshoot and collapse is a problem that many smaller economies have

encountered over the years. If I am right that we are now encountering a

similar situation, there is a big change ahead. The change will not be

instantaneous, however. The big question that arises is, “Over what time

scale does such a collapse take place?” If it takes place over a number

of years, it may look more like “overshoot and decline” than “overshoot

and collapse” to those who are living through the era.

A recent partial collapse was that of the Soviet Union in 1991. The

Soviet Union was an oil exporter. Oil prices had hit a high in 1981 and

had been declining for 10 years when the Soviet Union collapsed. With

low oil prices, it had been difficult to earn enough revenue to reinvest

in new oil fields to replace the production that naturally declines as

oil is extracted. Oil, directly and indirectly, had provided many jobs

for the Soviet Union. After ten years of stress, the central government

of the Soviet Union collapsed in 1991.

Low oil prices first slowed production growth between 1982 and 1987

(Figure 2). Oil production began to decline in 1988, three years before

the government collapsed. Production gradually rose again in the early

2000s, as oil prices rose again.

Figure 2. Oil production and price of the former Soviet Union (FSU), based on BP’s Statistical Review of World Energy 2015.

What was surprising to me was the fact that consumption

of all types of energy by the Soviet Union fell at the time of the

central government collapse in 1991, even hydroelectric. The overall

level of energy consumption never bounced back to its previous level.

Figure 3. Former Soviet Union energy consumption by fuel, based on data of BP’s Statistical Review of World Energy 2018.

What happened was that many inefficient industries were forced to

close. Some of these industries were in the Ukraine; others were in

Russia and elsewhere. As they closed, less electricity and less oil and

gas were used.

The loss in energy consumption was pretty much permanent. The

manufacturing that left the Soviet Union was replaced by other, more

efficient, manufacturing elsewhere. Also, without their previous

manufacturing jobs, the people of the former Soviet Union were poorer.

They could not afford to buy cars and homes, keeping fuel consumption

lower.

Another indicator regarding the speed of collapses is the analysis

done by researchers Peter Turchin and Sergey Nefedov, regarding

collapses of eight agricultural economies from earlier periods. I

compiled the information they provided in the book Secular Cycles in

the chart shown in Figure 4. In the cycles they analyzed, the “crisis

period” seemed to last 20 to 50 years. One thing that is striking in

their analysis is that epidemics often played a major role in the

declines. As wages disparity grew, poorer workers ate less well. They

became more vulnerable to epidemics and often died.

Figure 4. Chart by author based on information provided in Turchin and Nefedov’s book, Secular Cycles.

In these early cycles, the major industry was farming. These

collapses were in the days before electricity use. In these situations,

collapses tended to play out over 20 to 50 years. Our more modern

economy, with its just-in-time supply lines, would seem likely to

collapse more quickly, but we can’t know for certain. This analysis is

thus another data point that suggests that what may be ahead could be

closer to “overshoot and decline” than “overshoot and collapse.”

[C] What May Be Ahead

[1] We are likely to experience the collapse of central

governments of several of the oil exporting nations, in a manner not

entirely different from the collapse of the Soviet Union in 1991.

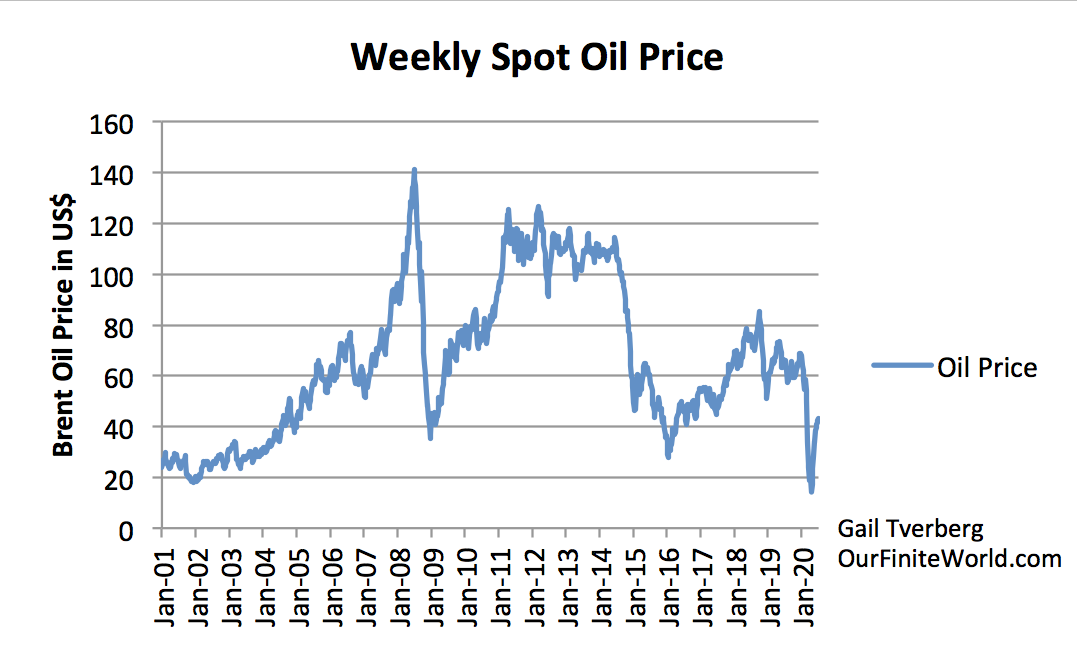

Oil prices have been low for a very long time, since 2008, or at least since 2014.

Figure 5. Weekly average spot oil prices for Brent, based on data of the US Energy Information Administration.

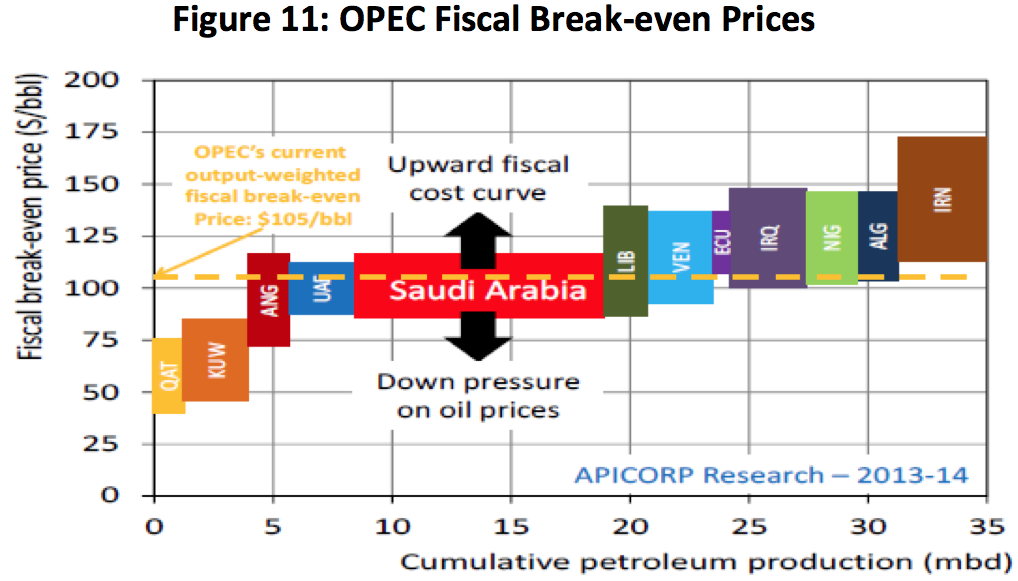

Most OPEC oil producers seem to require prices in the $100+ per

barrel range in order to be able to fund the programs their people

expect (Figure 6). One important program provides subsidies for imported

food; other programs provide jobs. Without these programs, revolutions

to overthrow the current leaders seem much more likely.

Figure

6. Estimate of OPEC break-even oil prices, including tax requirements

by parent countries, from APICORP. Figure is from 2014.

At this point, oil prices have been below $100 per barrel since 2014,

a period of 6 years (Figure 5). Stress is increasing; OPEC producers

have cut production in an attempt to try to get prices up. Prices are

now in the low $40s.

We should not be surprised if, over the next few years, oil

production starts to fall in several areas around the world because of

internal problems. Another possible impetus for the drop in production

may be wars with other nations. Some such wars might be started simply

to try to get the price of oil up to a more acceptable level.

We have been falsely led to believe that oil is not important;

renewables can handle our needs in the future. In fact, oil is essential

for today’s farming. It is essential for transportation of goods and

services of all kinds. It is essential for the construction industry and

for mining. Researchers in academic institutions have received grants,

encouraging them to put together models regarding what could be ahead.

These models tend to be extremely unrealistic.

One of the most absurd models is by Mark Jacobson.

He claims that by 2050, the world economy can operate almost entirely

using wind, solar, and hydroelectric. Unfortunately, we don’t have until

2050; world oil, coal, and natural gas supplies look likely to decline in the 2020 to 2025 timeframe because of low prices. Another problem with this approach is that there

is not very much fossil fuel to extract, because most of what appears

to be available from resource studies cannot really be extracted at the

low prices set by physics.

The underlying problem is confusion about which direction prices go,

as an economy reaches limits. Economists assume that scarcity will cause

prices to rise; the real story is that fossil fuel prices are set by the laws for physics because the economy is a dissipative structure. As the economy approaches limits, prices tend to fall too low for producers, rather than rise too high for consumers.1 The

sad truth is that we can’t even count on the continued extraction of

the small amount of fossil fuels that Jacobson assumes will exist after

2050.

[2] We are likely to see a huge change in the international

financial system and in the international trade system in the next few

years.

As long as there were plenty of resources, relative to the world

population, the optimal approach was to do as much international trade

as possible. This approach would maximize world GDP. It would also add

jobs in developing areas of the world without too huge an impact on jobs

availability in the countries moving their manufacturing to lower-cost

areas.

In the last few years, it has become increasingly evident that there

aren’t enough jobs that pay well to go around. This is really the

underlying problem with respect to the increased hostility among

nations, such as between the US and China. Tariffs are being used to try

to bring jobs that pay well back to those who need them. Strange as it

may seem, it takes fossil fuels to create jobs that pay well.

Figure 7. World Trade as a percentage of GDP, based on data of the World Bank.

Figure 7 shows that international trade was rising as a percentage of

GDP for many years, and it hit a high point in 2008. Since then it has

bounced around a little below that high point. In 2020, it will clearly

take a big step down because of all of the cancellation of trade related

to COVID-19 restrictions.

We saw earlier that commodity prices tend to fall too low for

producers. Indirectly, this means that profits tend to fall too low.

Interest rates tend to follow these low profits down, since businesses

cannot afford to pay high interest rates.

With these low profits and low wages, the financial system gets

strained. “Debt and more debt” seems to be the way to fix the system.

Growing debt at ever-lower interest rates is encouraged. These low

interest rates tend to raise asset prices because monthly payments to

buy these assets fall with the falling interest rates. Stock markets

tend to rise, even when the economy is doing poorly.

If the many strange approaches I outlined in Section A are used to

add even more debt to keep the system afloat, eventually some part of

the system is going to “break.” For example, banks will stop issuing

letters of credit with respect to purchases made by buyers that don’t

seem sufficiently creditworthy. Banks may stop trusting other banks,

especially if the banks do not really seem to be solvent. At some point,

the international financial system seems likely to start “coming

apart.” Eventually, the US dollar will stop being the world’s reserve

currency.

My guess is that a new two currency system will develop. Governments

will issue a lot of currency for local use. It will not be useful for

buying goods from other countries. Much of it will be used for buying

locally produced food and other locally produced goods.

Very little international trade will be done. Any international trade

that will be done will occur between trusted partners, at agreed upon

exchange rates. Perhaps a special currency will be used for this

purpose.

In this new world, individual countries will be very much on their

own. With very little fossil fuel, countries will tend to lose

electricity availability very quickly. Transmission lines will go

unrepaired. It will become impossible to fix existing wind turbines.

Road repair will become impossible. Electric cars will likely be as

unusable as gasoline powered ones.

There will likely be fighting about resources that are available,

leading to countries subdividing into smaller and smaller units,

hoarding what little resources they have available.

Note:

1Energy prices tend to fall too low because, as the

economy gets more complex, wage and wealth disparity tend to grow,

reflecting differences in training and responsibility. The problem

occurs because low-paid workers cannot afford to buy very large

quantities of goods and services produced by the economy. For example,

many cannot afford a car or a home of their own. The spending of

high-paid workers does not offset the loss of demand by low-paid workers

because high-paid workers tend to spend their wages more on services,

such as advanced education, which require proportionately less energy

consumption. Ultimately, the lack of demand by low-paid workers tends to

pull down the prices of oil and other commodities below the level

required by producers.

....

Add to this the quickly increasing catastrophic climate change events, growing tensions between nuclear armed powers which could easily ( almost happened already numerous times ) precipitate an extinction level event, the drastic loss of animals, fish, insects, rising ocean levels which will decimate coastlines and their human built infrastructure, etc, etc, the list of converging dire repercussions is very long.