https://peakoil.com/consumption/the-first-global-inflationary-depression-is-very-possible

The First “Global Inflationary Depression” Is Very Possible

It is possible that we might soon be witness to the first global inflationary depression. This is not a mix of words we normally see placed together. Several factors make this scenario possible. First, we seldom have depressions but instead, tend to roll through mild recessions, however, what we face may be far more severe. Second, in the past, times of falling economic activity have generally been deflationary as defaults rise but this time, not so much. Third, but not least, in the past, many events tended to be regional rather than global, but over the years as economies have become more interconnected the resulting codependency presents an increased possibility of problems spreading across the world.

Currently, the biggest source of demand comes from governments and not working people earning a living or businesses growing. If you remove all the money being spent on Covid-19 vaccinations, tests, and a slew of inefficient spending that has created little long-term benefits to the economy the GDP would fall like a stone. The money flowing from the central banks and governments has created the so-called “pent up demand” we have been hearing about and predictions of 5% or more GDP growth next year. In truth, capacity utilization is down even while trillions of new dollars pour into the system. This is the logic behind saying a depression may be in the wings.

China’s Economy Shows Signs Of Slowing

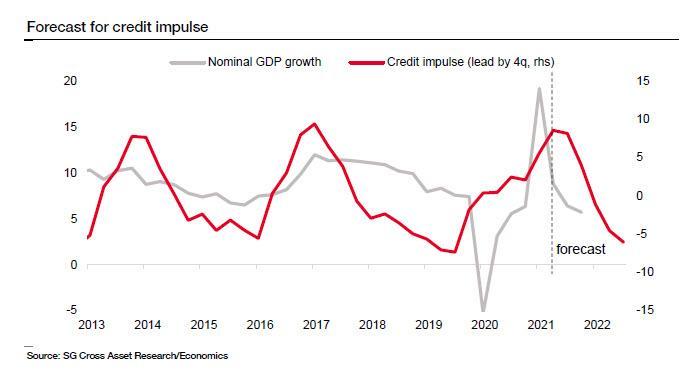

Recently several articles have appeared indicating the big boost China experienced post-Covid-19 has come to an end. China’s economy was the first to recover from the Covid-19 collapse due to trillions of credit pumped into the economy at home as well as Americans rushing out to buy imported goods using stimulus money. With China again showing signs of economic weakness, the story that it takes more and more stimulus to create the same kick each time we play this game is playing out. Back in December after a tremendous surge, China’s massive credit growth peaked resulting in SocGen forecasting a big slump was coming.

Across the world, sophisticated lenders, but not the general public, understand the history of how governments’ monetary policies destroy the purchasing power of currencies. To avoid the issue of currency debasement risk, regardless of the yield we have seen the power of being the world’s reserve currency on display in loan documents. Some 48% of the world’s $30T in cross-border loans are priced in US dollars, The BIS reports this is up from 40% a decade ago. This is why the dollar will most likely fare better than the euro or yen when fiat currencies come under assault.

The point is, inflation expectations are continuing to grow and the law of diminishing returns is raging havoc with the efforts of central banks to control the economy. This has resulted in investors moving into assets likely to do well in an inflationary environment. This can be seen in the way commodities, precious metals, and cryptocurrencies such as bitcoin have risen in favor with those seeking alternatives to more conventional investments. The continued appointment of dovish and easy money advocates to positions in high finance does little to reinforce confidence in the fiat currencies on which we rely.

Inflation is a form of theft that moves wealth from the people and into governments’ coffers. While many investors are focused on yield curves, bitcoin, and surging market valuations, the foundation of central bankers’ argument that more QE is possible without inflation may be crumbling. We are now seeing that large sectors of the economy are broken. Cryptos are jumping and some hedge-funds are suffering the greatest stock short-squeeze in history. This has forced these hedge-funds to liquidate many of their most liquid long positions.

Inflation Hits In An Uneven Manner

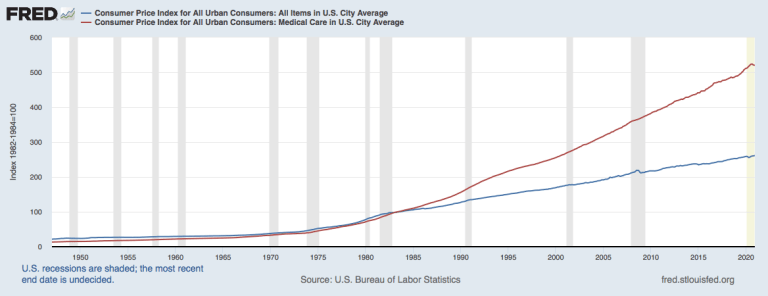

With this in mind, it is important to remember inflation does not occur at the same rate for all the commodities and services that affect our lives. This can be seen in the chart on the right. It shows the health care system in the United States has allowed its higher costs to flow through to consumers. This has resulted in much higher medical care costs for the consumer than the inflation implied by the Consumer Price Index. Figures, such as the CPI and GDP produced by the government are heavily skewed to reassure a docile populace that all is well.

Growing concern over the debasement of the fiat currencies issued by nations and central banks is adding to expectations inflation is waiting in the wings. Policies such as we see today would have been impossible when money was tied to gold. As investors shift into assets that do well during times of inflation, It is possible they will set in motion a self-feeding loop or cycle. When fiat money that has quietly sat in paper promises begins to be exchanged for tangible assets and inflation hedges it has the potential to reverse the long falling velocity of money.

Inflation brings with it higher interest rates which generally hit many sectors of the economy and puts a spotlight on the difference between liquidity and solvency. As interest rates rise construction tends to grind to a halt. Higher interest rates also result in people having a difficult time paying for or financing big-ticket items such as automobiles. In short, it puts a great deal of stress on all parts of the economy including the government deficits that have exploded since the 2008 financial crisis.

Two often-overlooked factors support the idea we are headed down a path of inflation even if the economy drastically slows. The first is many laws have been set in place to raise the minimum wage. The second is the fact that so many Americans work for the government. These are mostly full time and workers seldom get laid-off without pay. Figures from the National Debt Clock show just under 150 million workers are in the workforce and nearly 24 million of them are employed by the government. That is almost one in six. The government’s oversized role in today’s economy which is much larger than it was during the Great Depression has put a net under the ability of prices to fall.

In the past, there existed a pathway for deflation to take hold due to rising defaults as debt became unbearable but this is far less likely today. This is because several safety valves have been put into the system over the years. These are evident in the way bankruptcies take place, companies are now factoring in more bad debt in their price structure and last but not least an attitude governments and central banks should step in and save large businesses and institutions in danger of failure. Many people see this as a good thing but it has also led to the zombification of problems that artificially low-interest rates have only made worse. Masking the fact many companies and pension funds are insolvent has not made the economy stronger.

This all folds into the story of how for decades the monetary illusion created by central banks collaborating with governments has delayed an inevitable crisis by not dealing with reality. This means when the forces pent-up over the years finally break free events will most likely occur faster with far deeper ramifications than many people expect. When imbalances are ignored, bad things occur. When things finally blow up in the faces of those creating and promoting MMT we can expect to hear them claim it was not their fault and it was because of a general misunderstanding of the role of money and credit in the economy.

All of this is likely to have profound consequences for various inflation-sensitive assets around the world. The one thing we can count on is that when things crumble, the old, “we should have done more” or the “it would have been far worse” lines will flow forth. Those in charge often find great comfort in spouting such nonsense. We have been lulled into complacency and have given central banks too much credit for being able to control the economy and stop financial crises. The first global inflationary depression may not start today or tomorrow but it is coming and when it arrives most people will have never seen it coming.

....

https://www.blacklistednews.com/article/79143/avoid-the-great-reset-in-three-easy.html

There are two things that should be understood about the global financial markets as the world faces what is being called the Great Reset, or Bretton Woods 2.

The first is that the US dollar rules the world (as distinct from the US nation).

The second is that the system is insane.

Sure, it may look rational with all those numbers, charts, ratios, algorithms and impressive-sounding technical terms. But collectively the whole thing is mad. As the great British writer GK Chesterton said:

The madman is not the man who has lost his reason. The madman is the man who has lost everything except his reason.

That nicely describes the global capital markets and it does not bode well either for an effective reset or the survival of the monetary system itself.

The US dollar has dominated the global financial markets since 1945, when Franklin D Roosevelt did a deal with King Abdulaziz of Saudi Arabia to denominate oil trade in the American currency, leading to the creation of the ‘petrodollar’ which then became the world’s reserve currency.

The petrodollar has long since faded; more oil is actually denominated in Chinese yuan now than American dollars (although the yuan is fixed to the US dollar so it is not really separate). But the bulk of international trade and asset buying is still denominated in US dollars out of habit and the US dollar has been further entrenched because of the emergence of the global derivatives market. Derivatives are transactions derived from, or rather are gambles on, conventional financial assets such as currencies, interest rates and shares.

The ‘value’ (whatever that means exactly) of these derivatives is $US500-1000 trillion, give or take the odd $US100 trillion.

This intense financial activity, most of which occurs in microseconds, is like having a massive roulette wheel spinning above the earth. According to the Bank for International Settlements, the daily cross border trades with the US dollar on one side equates with almost $US6 trillion.

To give some idea of how big that notional ‘money’ is, the entire US Federal debt, built up over decades, is about $US27 trillion, or the equivalent of less than five days trading. It has entrenched the US dollar as the world’s reserve currency and allows America to do whatever it likes on its Federal budget, its military spending or whatever other financial excesses it can devise, such as a $US21 trillion hole in the defence budget.

Whatever debt the US issues is swallowed up by the massive demand for dollars in the foreign exchange markets. No other country has that freedom.

It has recently become popular to criticise so-called ‘fiat money’, money that is determined by government edict. The contention is that when President Richard Nixon took America off the gold standard in 1971, because the nation could not pay for the Vietnam War, it ushered in an era of government-created money whose value has been progressively degraded.

Though superficially persuasive the argument is entirely misleading. The repeated crises in the financial markets over the last four decades have not been because of too much government intrusion but the opposite: a refusal by governments to govern properly, which allowed private players to run amok.

It was a cleverly engineered scam.

In the 1980s and 1990s there was a world-wide push, prosecuted by well-funded think tanks and lobbyists, to ‘deregulate’ the financial markets. What nobody seemed to notice, or if they did notice they conveniently chose to ignore it, is that this argument is, literally, nonsense. It is impossible to deregulate financial markets because they consist of regulations. Deregulating financial markets is like trying to take the hydrogen, oxygen and wetness out of water. Other types of markets can be deregulated because regulations are external to the economic activity, but in finance they are the same.

Enter insanity.

By convincing Western governments that deregulation was a fine thing (usually using water metaphors to make it seem that regulations somehow got in the way of monetary ‘flows’) private actors were able to make up their own rules, triggering ‘financialisation’, or wealth extraction by the finance sector at the expense of everyone else.

The ridiculous invention of rules has been most obvious in the derivatives markets, which are a complete free-for-all – think of a bet, any bet. It also occurred in the real economy, where unshackled banks and financial institutions invented different ways to create ludicrous levels of global debt that are now, in aggregate, unpayable. The only option for central banks in developed countries has been to drop interest rates to almost zero in the hope of kicking the can down the street and printing money, known as ‘quantitative easing’, on what is laughably called their ‘balance sheets’.

There were plenty of warnings that ‘deregulation’ was dangerous. In 1998, a derivatives company, Long Term Capital Management nearly brought down the Western banking system. Bizarrely, the chairman of the US Federal Reserve, Alan Greenspan, responded by aggressively increasing the number of derivatives traders in the belief that it would all, sort of, balance itself out.

It didn’t.

The 2007-2008 financial crisis revealed the insanity of allowing private players to invent their own rules when there was a near collapse of the entire system. It was only saved because the US Treasury head, Henry Paulson, decided to re-regulate instead of standing back and allowing ‘market forces’ to work.

It was a close run thing, though. On September 18, 2008, $US550 billion went out of the US money markets in a couple of hours. Paulson responded by closing down all America’s money accounts and announcing a guarantee of $250,000 for all bank deposits. That is, he issued a fiat. The Treasury later estimated that had he not done so $US6 trillion would have exited the US financial system by the end of the day. Given that banks lend out roughly 20 times their capital base this would have spelt the end of the monetary system of the world.

Like all good madmen, banks and financial traders, incapable of taking any responsibility for their own actions and faithfully adhering to their smug anti-government rhetoric, outrageously blamed governments for a crisis that they had caused. They got away with it. Almost no financiers went to jail and they continued their debauch of the system, exploiting lower interest rates to increase debt to its current unsustainable levels.

Can a genuine reset be achieved? Not with the current finance technocrats, who have probably never scrutinised an assumption in their lives. Compare these superficial thinkers with John Maynard Keynes, the person who led the British delegation to Bretton Woods 1 in 1944. A member of the Bloomsbury Group Keynes thought deeply both about what money is and how it should function (he is associated with the economics of government spending but that is only a cartoonish version of his thought). Almost none of the current crop of central bankers, heads of global institutions or schemers in the World Economic Forum are capable of such reflection. Most did not even notice that ‘financial deregulation’ is a flat contradiction....

No comments:

Post a Comment