https://wallstreetonparade.com/2020/01/bernie-sanders-hasnt-quite-captured-what-wall-street-does-its-actually-a-fraud-monetization-system-with-a-money-printing-unit-called-the-new-york-fed/

Bernie Sanders Hasn’t Quite Captured What Wall Street Does: It’s Actually a Fraud-Monetization System with a Money-Printing Unit Called the New York Fed

Senator Bernie Sanders has come closer than anyone on the Presidential campaign trail in defining what Wall Street actually does. Sanders has repeatedly stated at his rallies that “the business model of Wall Street is fraud.”

That analysis is correct but abbreviated. Sanders needs to go further. It’s not just Wall Street’s business model that has left the United States with the greatest wealth inequality since the Roaring Twenties (a time when Wall Street investment banks were also allowed to own deposit-taking banks). It’s how Wall Street is monetizing that fraud that poses an existential threat to the solvency of the United States and the impoverishment of millions of Americans.

The attempted WeWork Initial Public Offering (IPO) of last year was a classic example of how Wall Street can put lipstick on a pig, pass it off as a hot new startup company, and sell its shares, which were overpriced by about $40 billion, to unwary public pension funds and mutual funds that dominate millions of Americans’ 401(k) plans. The IPO failed to materialize simply because alternative media sent the dirty details of the offering viral, forcing business media to cover the story.

Rather than being a hot new tech startup with oodles of potential, WeWork was a money-losing real estate leasing company with a grifter as its CEO. That, however, didn’t stop two of the largest law firms, Skadden Arps, Slate, Meagher & Flom and Simpson, Thacher & Bartlett, from representing the company and the underwriters, respectively, and it didn’t stop two of the biggest firms on Wall Street, JPMorgan Chase and Goldman Sachs, from trying to unload the dog of a deal on investors for a hefty underwriting fee.

That’s what we mean by monetization of fraud. (See The Dickensian Tale of the WeWork IPO.)

Now you may be thinking that WeWork might have been just an aberration where due diligence slipped through the cracks by a bunch of overworked bean counters. Unfortunately, this is the way that Wall Street has been issuing IPOs for a very, very long time.

In 2003 the Securities and Exchange Commission settled charges against ten of the largest Wall Street firms over how their research analysts had been issuing fraudulent reports to the public on IPOs. The analysts were sending internal emails to colleagues calling the offerings “dogs” and “crap” while telling the investing public that these were great companies with bright futures and putting a “buy” recommendation on the stock.

Those fraudulent research reports and “buy” recommendations led to a $4 trillion bust in the stock market, known as the dot.com crash. While public pensions and individuals investors suffered enormous losses, the Wall Street analysts and their bosses got to keep their fat bonuses.

This is another example of long-running monetization of fraud schemes on Wall Street.

The epic financial collapse on Wall Street in 2008 was, reduced to its basic terms, simply the end game of Wall Street banks’ efforts to monetize their frauds. Insiders at the major Wall Street banks had told their bosses that the mortgage underwriting department was issuing mortgage loans to people who could not possibly afford to repay the loan. They warned their bosses to reject the loans. But they were overruled because the Wall Street banks had a grander scheme: they would make money securitizing the loans; they would make more money creating synthetic derivatives to bet on the loans; they would make even more money shorting the loans based on their insider knowledge that the loans were doomed to default; and they would make even more money allowing hedge funds to pay them to assemble these dogs into new securitizations so that they hedge funds could make billions shorting the pile of dung. (See here, here and here.)

The 2008 crash and the ensuing Great Recession were the worst economic disasters in the United States since the Great Depression. Millions of Americans lost their homes to foreclosure, millions more lost their jobs as a result of the economic contraction, and trillions of dollars of household wealth was wiped out.

The Financial Crisis Inquiry Commission (FCIC) issued a report attempting to capture for the American people what had gone so wrong on Wall Street and how Federal regulators and Congress had failed to catch the corruption in time to prevent the epic crash. If you were asked to give a one-sentence explanation for what happened on Wall Street from the findings of the FCIC report, you could do no better than this: Wall Street was monetizing fraud.

The dot.com bust in 2000 and the epic financial crash in 2008 were both the well-documented result of Wall Street monetizing its fraud and its execs and traders getting to keep the multi-million dollar salaries and bonuses that ensued from that fraud monetization.

The reason that Wall Street continues to be allowed by Congress to pursue its fraud monetization schemes is that Wall Street has captured both Congress and its federal regulators. A significant number of members of Congress are beholding to Wall Street to fund their political campaigns. Without that funding, the incumbent doesn’t stand a chance against their opponent, who will tell Wall Street what they want to hear and grab Wall Street’s funding. Federal regulators are either looking to return to their seven figure jobs on Wall Street or are auditioning to get one.

The revolving door has now even corrupted the accounting profession that audits our publicly-traded companies, as recently reported in-depth by The Project On Government Oversight. (See “How Accountants Took Washington’s Revolving Door to a Criminal Extreme.”)

But what would happen if a criminal network actually obtained a government power to financially resuscitate itself after each of its crime waves? Wouldn’t that make it the most dangerous threat to national security?

On April 9, 2019, the nonprofit Wall Street watchdog, Better Markets, released a study titled: “Wall Street’s Six Biggest Bailed-Out Banks: Their RAP Sheets & Their Ongoing Crime Spree.” It should have made headlines on the front pages of every major newspaper in the U.S. Instead, it was effectively ignored by mainstream media.

The report notes this:

“Of the more than $29 trillion in bailouts, just the six biggest banks in the country (the ‘Six Megabanks’) received more than $8.2 trillion in lifesaving support from American taxpayers during the 2008 financial crash, or nearly one-third of the total bailouts provided to the entire financial system. This was a massive transfer of wealth from Main Street to Wall Street to prevent the bankruptcy of just six banks, supposedly because they were vital to the economic security and prosperity of Main Street Americans.”

Who provided the bulk of that $29 trillion in bailout money to resuscitate banks engaged in serial frauds? It was the New York Fed, another captured regulator with one critically important and critically dangerous difference from other regulators: it has the ability to electronically create money out of thin air.

As a sign of just how brazen and disastrously broken the U.S. financial system has become, with no hearings in Congress, with no blaring headlines on the front pages of newspapers, the New York Fed turned on its money spigot to Wall Street again on September 17, 2019. It was the first time this has happened since the financial crisis. For the past four months the New York Fed has been spewing hundreds of billions of dollars each week to Wall Street’s trading houses, pushing the Dow Jones Industrial Average up by 3,000 points, with no accountability to anyone or explanation as to why Wall Street needs or deserves this money.

Americans must engage in demanding accountability from their elected, and as yet uncaptured, members of Congress.

....

https://wallstreetonparade.com/2021/02/within-a-matter-of-months-the-feds-balance-sheet-will-hit-8-trillion-these-charts-tell-the-re

Within a Matter of Months, the Fed’s Balance Sheet Will Hit $8 Trillion; These Charts Tell the Rest of the Story

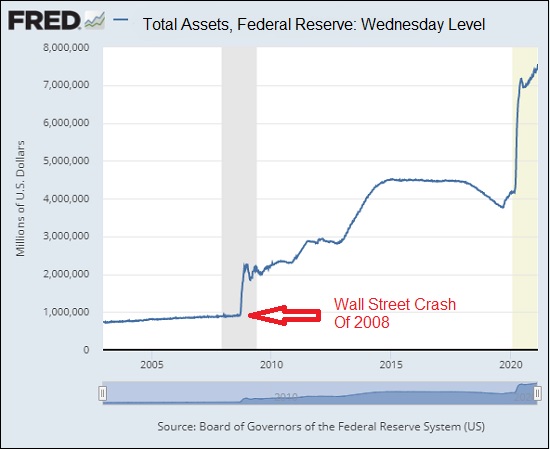

Every Thursday, at approximately 4:30 p.m., the Federal Reserve provides a report on its balance sheet as of the prior day. It’s known as the H.4.1 report or the Wednesday Level report.

On Thursday, September 4, 2008, the Fed’s H.4.1 report showed a $935 billion balance sheet as of Wednesday, September 3, 2008. That was 12 days before iconic financial institutions on Wall Street began to blow up in what became the worst financial crisis since the Great Depression. As of last Wednesday, February 17, 2021, the Fed’s balance sheet stood at $7.6 trillion – an increase of 712.83 percent in less than 13 years.

The Federal Reserve was created in 1913 and such a staggering growth in its balance sheet has not occurred at any other period in U.S. history — not during the Great Depression, not even during or after World War II.

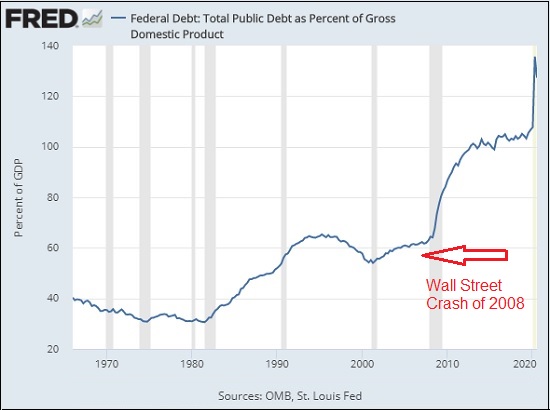

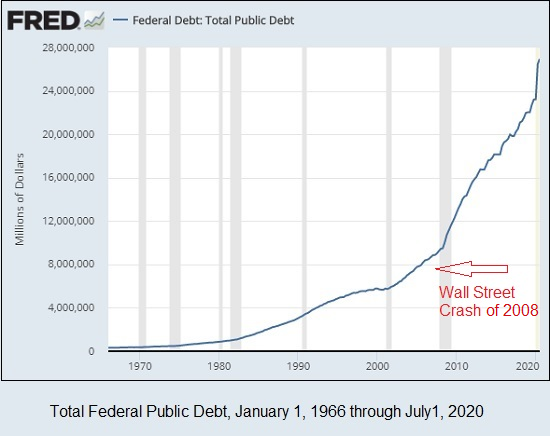

What has changed the course of economic history in the United States and put the country on a debt-fueled disaster course is the Wall Street crash of 2008 and the bailouts, both monetary and fiscal, that have followed ever since, together with the unwillingness of Congress to confront this reality.

The charts above showing the unprecedented growth in the federal debt and federal debt versus GDP since the Wall Street crash of 2008 confirm this thesis.

Among the many factors that have kept the U.S. locked on this destructive debt path are the following:

The failure by Congress to separate the giant federally-insured banks from the Wall Street casino, that is, to restore the Glass-Steagall Act, thus making perpetual Wall Street bailouts unnecessary;

The failure by Congress to strip federally-insured banks of the ability to hold tens of trillions of dollars notionally in dangerous derivatives, thus making perpetual bailouts unnecessary;

The fear by the Fed of allowing another stock market crash because consumers might retrench from spending if their 401(k)s implode;

The failure by Congress to restore corporate pension plans to workers, thus allowing loyal, productive U.S. workers to live in dignity in their retirement years and de-linking the wealth effect from the stock market and 401(k) plans;

The failure by Congress to conduct meaningful forensic investigations into how Wall Street’s Dark Pools, High Frequency Traders, and mega banks have joined forces to become a fraud monetization system and institutionalized wealth transfer mechanism, creating the worst wealth and income inequality in U.S. history.

Time is running out for Congress to act.

No comments:

Post a Comment